Why Traditional Recession Signals Broke — and the Role of Liquidity Since 2020

For decades, investors relied on a familiar playbook:

An inverted yield curve

A falling Leading Economic Index (LEI)

A recession shortly after

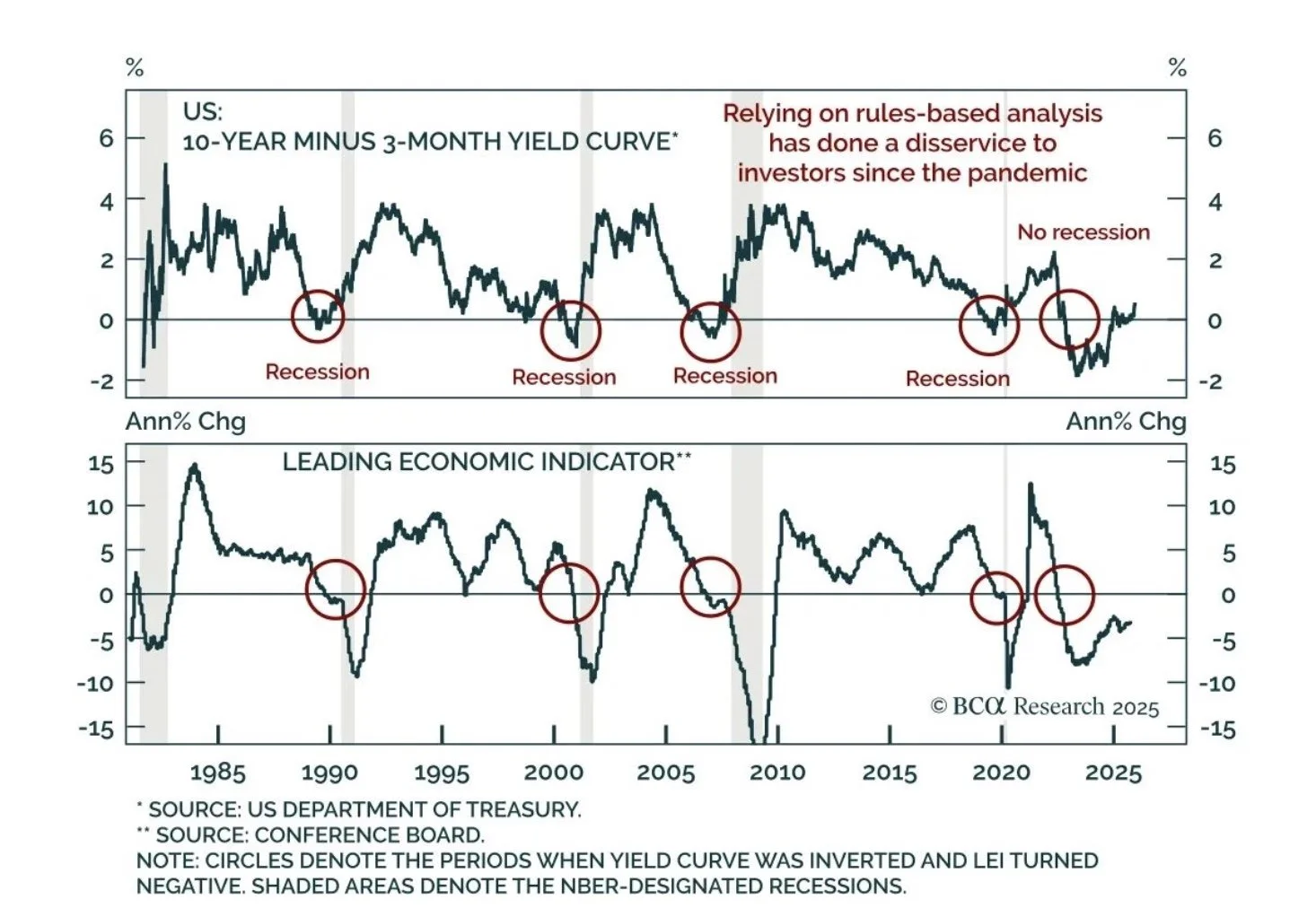

Historically, this framework worked remarkably well. The chart above illustrates that pattern clearly — yield curve inversions and negative LEI readings consistently preceded U.S. recessions for nearly forty years.

But since the pandemic, that relationship has fractured.

Despite one of the longest yield curve inversions on record and a deeply negative LEI, the U.S. economy has not entered a traditional recession. To understand why, we need to examine a variable that prior cycles didn’t contend with at this scale: extraordinary liquidity.

The Yield Curve: A Signal, Not a Cause

The yield curve reflects expectations about future growth and monetary policy. When short-term rates rise above long-term rates, it typically signals that financial conditions are tightening and growth may slow.

Before 2020, tighter conditions often meant:

Reduced bank lending

Higher borrowing costs

Less capital available to households and businesses

That transmission mechanism is what historically led from inversion → slowdown → recession.

However, the yield curve does not operate in isolation.

Liquidity Changed the Transmission Mechanism

Following the pandemic, the U.S. economy experienced an unprecedented wave of liquidity from both fiscal and monetary channels, including:

Large-scale fiscal stimulus

Direct household transfers

Expanded unemployment benefits

Corporate credit backstops

Bank reserve expansion

Emergency lending facilities

Balance sheet expansion by the Federal Reserve

This liquidity fundamentally altered how higher interest rates flowed through the economy.

Instead of capital becoming scarce:

Households entered the cycle with excess savings

Corporations refinanced debt at historically low rates

Banks remained well-capitalized

Credit continued flowing even as policy tightened

In other words, rates rose — but liquidity never truly left the system.

Why the Leading Economic Index Also Struggled

The LEI aggregates forward-looking indicators such as manufacturing orders, credit conditions, and financial market signals. In prior cycles, a sustained negative LEI almost always coincided with recession.

Yet post-2020:

Liquidity muted downside volatility

Labor markets remained unusually tight

Consumer balance sheets stayed resilient

Government spending offset private-sector slowing

The LEI correctly captured slowing momentum, but it overstated the probability of outright contraction because it could not fully account for policy-driven demand support.

Rules-Based Models vs. Policy-Driven Cycles

The key lesson from the chart is not that economic indicators are useless — it’s that rules-based analysis struggles in policy-dominated environments.

When:

Central banks actively manage liquidity

Governments deploy fiscal tools counter-cyclically

Markets anticipate intervention

Traditional cause-and-effect relationships weaken.

This does not eliminate cycles, but it changes their shape:

More rolling slowdowns

Fewer deep contractions

Longer transitions between regimes

Higher dispersion across sectors

What This Means for Investors

Relying solely on historical recession signals can lead to costly decisions, particularly when liquidity conditions override traditional constraints.

A more adaptive framework focuses on:

Liquidity flows, not just interest rates

Balance sheet health of consumers and corporations

Credit availability, not only credit cost

Fiscal policy alongside monetary policy

In modern markets, liquidity is often the binding constraint — not rates alone.

Bottom Line

The yield curve and LEI remain valuable tools, but they are no longer sufficient on their own. Since the pandemic, aggressive central bank and government intervention has reshaped economic outcomes, delaying or softening downturns that traditional models would have predicted.

Understanding why the signals failed is more important than dismissing them entirely.

Markets evolve. Frameworks must evolve with them.

Disclosure:

This content is provided for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any security. The views expressed are as of the date of publication and are subject to change without notice. Past performance and historical relationships are not indicative of future results. All investing involves risk, including the possible loss of principal. This material does not take into account the specific financial circumstances, objectives, or needs of any individual investor. Investors should consult a qualified financial professional before making investment decisions.